")

[ad_1]

Douglas Rissing

The jobless fee noticed an sudden decline in September, falling to three.5% from 3.7%.

That took the wind out of the gross sales of the Fed Pivot crowd, who had been hoping that additional proof of abrasion within the labor market after the plunge in job openings reported earlier this week. Labor drive participation the explanation for decrease unemployment, ticking all the way down to 64.7% from 64.8%.

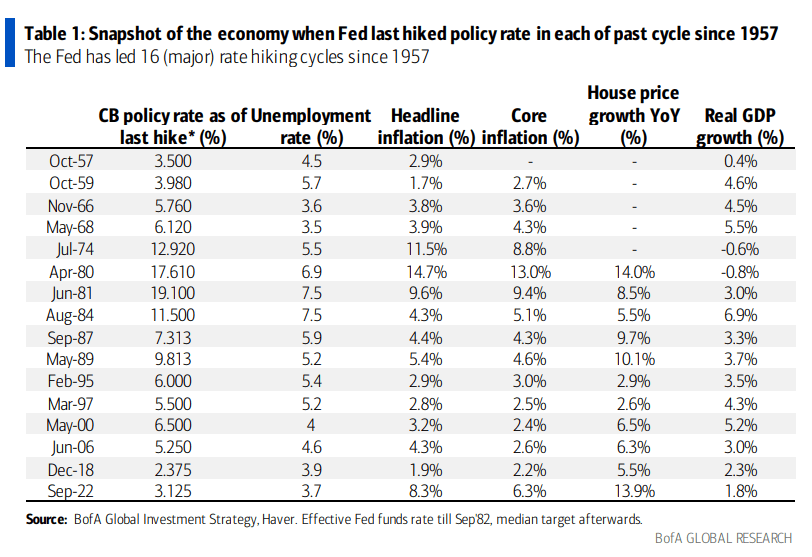

Previously 60 years there have been 15 Fed rate-hiking cycles and the common unemployment fee on the time of the final Fed fee hike was 5.7%, BofA strategist Michael Hartnett mentioned.

1")

Whereas previous occasions aren’t any predictors of future occasions, if that pattern continued the jobless fee would now be greater than 200 foundation factors away from a Fed end. If the Fed is actually dedicated to bringing down inflation to 2%, that reinforces the chance of a tough touchdown the place the last word highs in credit score spreads (LQD) (JNK) and supreme lows in shares (NYSEARCA:SPY) (QQQ) (DIA) (IWM) have but to be seen, Harnett mentioned.

The vitality markets (USO) (BNO) (UNG) are merely manner too robust for a 3% fed funds fee to deliver down inflation, Hartnett added.

Wanting close to time period, Harnett leans to danger seeing new lows in This fall as “coverage ‘panics’ fail” and a mix of latest lows for the yen, U.Ok. gilts “amazingly” rising once more regardless of BoE QE and a bond crash prefacing an upcoming recession “places downward stress on EPS, shares, company bonds.”

Occasions favoring danger rallying in This fall can be “markets rebelling towards QT,” the S&P ground of three,600 and 10-year Treasury yield (TBT) (TLT) ceiling of 4% holding, a triggering of monetary systemic worry, coverage motion (BoJ/BoE/RBA) and cracks in U.S. labor market and housing market engendering “renewed hopes Fed reducing charges towards end-2023,” he mentioned.

It’s “so tempting to be contrarian bull (bonds have crashed, US shares buying and selling 15X ahead earnings, everybody bearish; we all know yield curve says recession and yield curve all the time appropriate (see 13 of previous 13 inversions),” he added.

Source link